I am pleased to announce the blorr package, a set of tools for building and validating binary logistic regression models in R, designed keeping in mind beginner/intermediate R users. The package includes:

- comprehensive regression output

- variable selection procedures

- bivariate analysis, model fit statistics and model validation tools

- various plots and underlying data

If you know how to build models using glm(), you will find blorr very

useful. Most of the functions use an object of class glm as input. So you

just need to build a model using glm() and then pass it onto the functions in

blorr. Once you have picked up enough knowledge of R, you can move on to

more intuitive approach offered by tidymodels etc. as they offer more

flexibility, which blorr does not.

Installation

# Install release version from CRAN

install.packages("blorr")

# Install development version from GitHub

# install.packages("devtools")

devtools::install_github("rsquaredacademy/blorr")Shiny App

blorr includes a shiny app which can be launched using

blr_launch_app()or try the live version here.

Read on to learn more about the features of blorr, or see the blorr website for detailed documentation on using the package.

Data

To demonstrate the features of blorr, we will use the bank marketing data set. The data is related with direct marketing campaigns of a Portuguese banking institution. The marketing campaigns were based on phone calls. Often, more than one contact to the same client was required, in order to access if the product (bank term deposit) would be (‘yes’) or not (‘no’) subscribed. It contains a random sample (~4k) of the original data set which can be found at https://archive.ics.uci.edu/ml/datasets/bank+marketing.

Bivariate Analysis

Let us begin with careful bivariate analysis of each possible variable and the outcome variable. We will use information value and likelihood ratio chi square test for selecting the initial set of predictors for our model. The bivariate analysis is currently avialable for categorical predictors only.

blr_bivariate_analysis(bank_marketing, y, job, marital, education, default,

housing, loan, contact, poutcome)## Bivariate Analysis

## ----------------------------------------------------------------------

## Variable Information Value LR Chi Square LR DF LR p-value

## ----------------------------------------------------------------------

## job 0.16 75.2690 11 0.0000

## marital 0.05 21.6821 2 0.0000

## education 0.05 25.0466 3 0.0000

## default 0.02 6.0405 1 0.0140

## housing 0.16 72.2813 1 0.0000

## loan 0.06 26.6615 1 0.0000

## contact 0.31 124.3834 2 0.0000

## poutcome 0.53 270.6450 3 0.0000

## ----------------------------------------------------------------------Weight of Evidence & Information Value

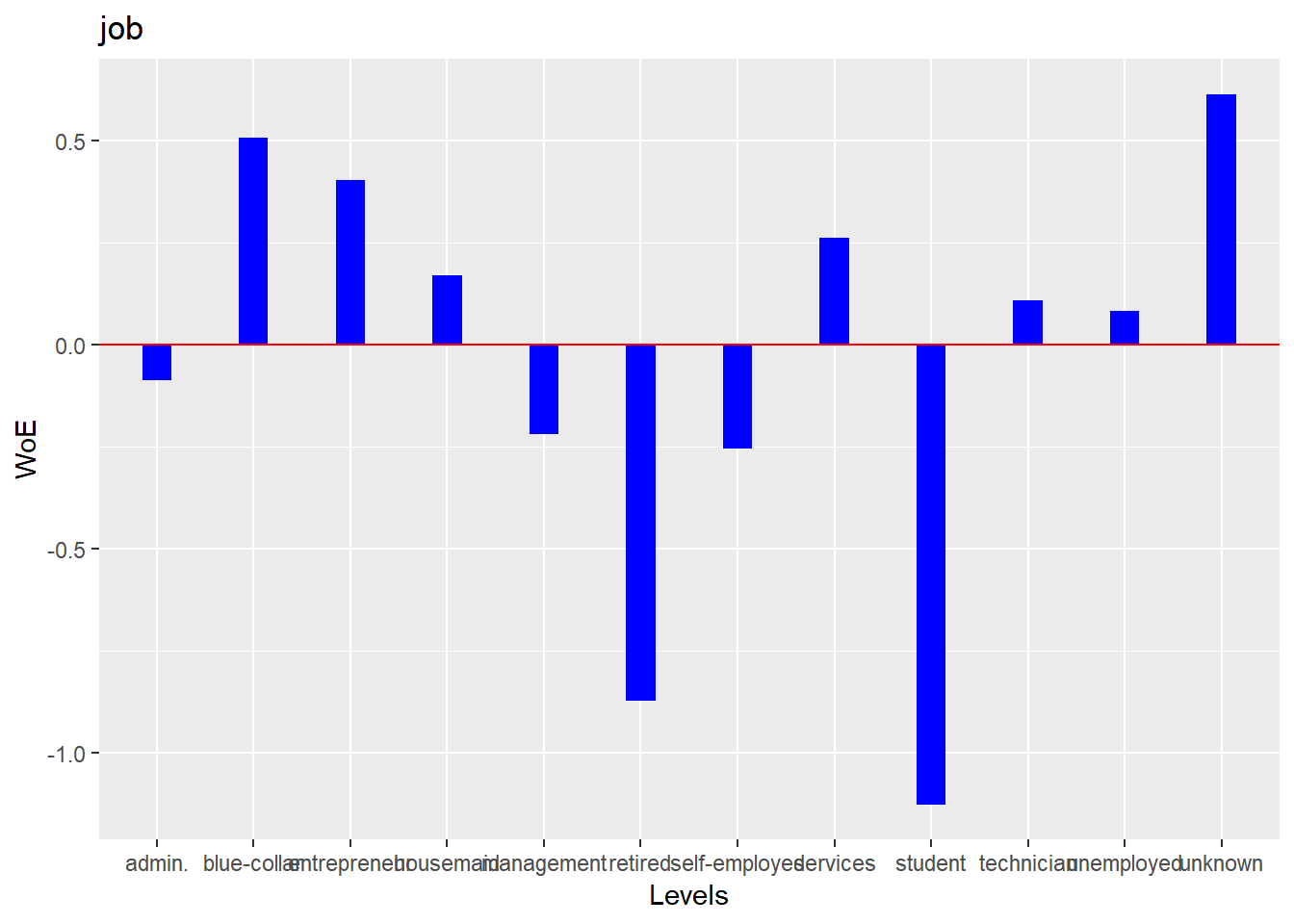

Weight of evidence (WoE) is used to assess the relative risk of di¤erent attributes for a characteristic and as a means to transform characteristics into variables. It is also a very useful tool for binning. The WoE for any group with average odds is zero. A negative WoE indicates that the proportion of defaults is higher for that attribute than the overall proportion and indicates higher risk.

The information value is used to rank order variables in terms of their predictive power. A high information value indicates a high ability to discriminate. Values for the information value will always be positive and may be above 3 when assessing highly predictive characteristics. Characteristics with information values less than 0:10 are typically viewed as weak, while values over 0.30 are sought after.

blr_woe_iv(bank_marketing, job, y)## Weight of Evidence

## --------------------------------------------------------------------------------

## levels 0s_count 1s_count 0s_dist 1s_dist woe iv

## --------------------------------------------------------------------------------

## management 809 130 0.20 0.25 -0.22 0.01

## technician 682 79 0.17 0.15 0.11 0.00

## entrepreneur 139 12 0.03 0.02 0.40 0.00

## blue-collar 937 73 0.23 0.14 0.51 0.05

## unknown 29 2 0.01 0.00 0.61 0.00

## retired 152 47 0.04 0.09 -0.87 0.05

## admin. 433 61 0.11 0.12 -0.09 0.00

## services 392 39 0.10 0.08 0.26 0.01

## self-employed 132 22 0.03 0.04 -0.26 0.00

## unemployed 126 15 0.03 0.03 0.08 0.00

## housemaid 110 12 0.03 0.02 0.17 0.00

## student 63 25 0.02 0.05 -1.13 0.04

## --------------------------------------------------------------------------------

##

## Information Value

## -----------------------------

## Variable Information Value

## -----------------------------

## job 0.1594

## -----------------------------Plot

k <- blr_woe_iv(bank_marketing, job, y)

plot(k)

Multiple Variables

We can generate the weight of evidence and information value for multiple

variables using blr_woe_iv_stats().

blr_woe_iv_stats(bank_marketing, y, job, marital, education)## Variable: job

##

## Weight of Evidence

## --------------------------------------------------------------------------------

## levels 0s_count 1s_count 0s_dist 1s_dist woe iv

## --------------------------------------------------------------------------------

## management 809 130 0.20 0.25 -0.22 0.01

## technician 682 79 0.17 0.15 0.11 0.00

## entrepreneur 139 12 0.03 0.02 0.40 0.00

## blue-collar 937 73 0.23 0.14 0.51 0.05

## unknown 29 2 0.01 0.00 0.61 0.00

## retired 152 47 0.04 0.09 -0.87 0.05

## admin. 433 61 0.11 0.12 -0.09 0.00

## services 392 39 0.10 0.08 0.26 0.01

## self-employed 132 22 0.03 0.04 -0.26 0.00

## unemployed 126 15 0.03 0.03 0.08 0.00

## housemaid 110 12 0.03 0.02 0.17 0.00

## student 63 25 0.02 0.05 -1.13 0.04

## --------------------------------------------------------------------------------

##

## Information Value

## -----------------------------

## Variable Information Value

## -----------------------------

## job 0.1594

## -----------------------------

##

##

## Variable: marital

##

## Weight of Evidence

## ---------------------------------------------------------------------------

## levels 0s_count 1s_count 0s_dist 1s_dist woe iv

## ---------------------------------------------------------------------------

## married 2467 273 0.62 0.53 0.15 0.01

## single 1079 191 0.27 0.37 -0.32 0.03

## divorced 458 53 0.11 0.10 0.11 0.00

## ---------------------------------------------------------------------------

##

## Information Value

## -----------------------------

## Variable Information Value

## -----------------------------

## marital 0.0464

## -----------------------------

##

##

## Variable: education

##

## Weight of Evidence

## ----------------------------------------------------------------------------

## levels 0s_count 1s_count 0s_dist 1s_dist woe iv

## ----------------------------------------------------------------------------

## tertiary 1104 195 0.28 0.38 -0.31 0.03

## secondary 2121 231 0.53 0.45 0.17 0.01

## unknown 154 25 0.04 0.05 -0.23 0.00

## primary 625 66 0.16 0.13 0.20 0.01

## ----------------------------------------------------------------------------

##

## Information Value

## ------------------------------

## Variable Information Value

## ------------------------------

## education 0.0539

## ------------------------------blr_woe_iv() and blr_woe_iv_stats() are currently avialable for categorical

predictors only.

Stepwise Selection

For the initial/ first cut model, all the independent variables are put into

the model. Our goal is to include a limited number of independent variables

(5-15) which are all significant, without sacrificing too much on the model

performance. The rationale behind not-including too many variables is that the

model would be over fitted and would become unstable when tested on the

validation sample. The variable reduction is done using forward or backward

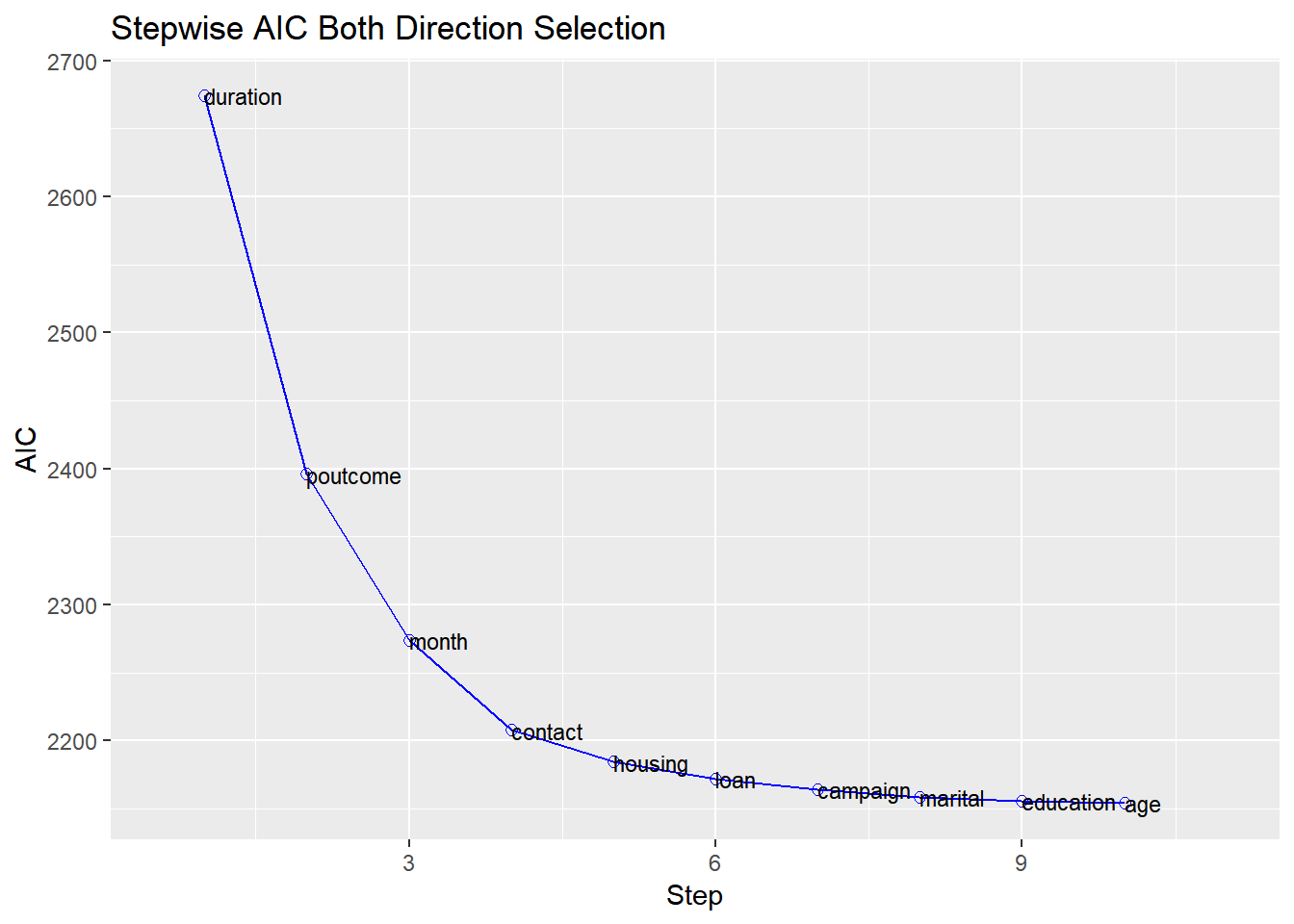

or stepwise variable selection procedures. We will use blr_step_aic_both()

to shortlist predictors for our model.

Model

model <- glm(y ~ ., data = bank_marketing, family = binomial(link = 'logit'))Selection Summary

blr_step_aic_both(model)## Stepwise Selection Method

## -------------------------

##

## Candidate Terms:

##

## 1 . age

## 2 . job

## 3 . marital

## 4 . education

## 5 . default

## 6 . balance

## 7 . housing

## 8 . loan

## 9 . contact

## 10 . day

## 11 . month

## 12 . duration

## 13 . campaign

## 14 . pdays

## 15 . previous

## 16 . poutcome

##

##

## Variables Entered/Removed:

##

## - duration added

## - poutcome added

## - month added

## - contact added

## - housing added

## - loan added

## - campaign added

## - marital added

## - education added

## - age added

##

## No more variables to be added or removed.##

##

## Stepwise Summary

## ---------------------------------------------------------

## Variable Method AIC BIC Deviance

## ---------------------------------------------------------

## duration addition 2674.384 2687.217 2670.384

## poutcome addition 2396.014 2428.097 2386.014

## month addition 2274.109 2376.773 2242.109

## contact addition 2207.884 2323.381 2171.884

## housing addition 2184.550 2306.463 2146.550

## loan addition 2171.972 2300.302 2131.972

## campaign addition 2164.164 2298.910 2122.164

## marital addition 2158.524 2306.103 2112.524

## education addition 2155.837 2322.666 2103.837

## age addition 2154.272 2327.517 2100.272

## ---------------------------------------------------------Plot

model %>%

blr_step_aic_both() %>%

plot()## Stepwise Selection Method

## -------------------------

##

## Candidate Terms:

##

## 1 . age

## 2 . job

## 3 . marital

## 4 . education

## 5 . default

## 6 . balance

## 7 . housing

## 8 . loan

## 9 . contact

## 10 . day

## 11 . month

## 12 . duration

## 13 . campaign

## 14 . pdays

## 15 . previous

## 16 . poutcome

##

##

## Variables Entered/Removed:

##

## - duration added

## - poutcome added

## - month added

## - contact added

## - housing added

## - loan added

## - campaign added

## - marital added

## - education added

## - age added

##

## No more variables to be added or removed.

Regression Output

Model

We can use bivariate analysis and stepwise selection procedure to shortlist

predictors and build the model using the glm(). The predictors used in the

below model are for illustration purposes and not necessarily shortlisted

from the bivariate analysis and variable selection procedures.

model <- glm(y ~ age + duration + previous + housing + default +

loan + poutcome + job + marital, data = bank_marketing,

family = binomial(link = 'logit'))Use blr_regress() to generate comprehensive regression output. It accepts

either of the following

- model built using

glm() - model formula and data

Using Model

Let us look at the output generated from blr_regress():

blr_regress(model)## - Creating model overview.

## - Creating response profile.

## - Extracting maximum likelihood estimates.

## - Estimating concordant and discordant pairs.## Model Overview

## ------------------------------------------------------------------------

## Data Set Resp Var Obs. Df. Model Df. Residual Convergence

## ------------------------------------------------------------------------

## data y 4521 4520 4498 TRUE

## ------------------------------------------------------------------------

##

## Response Summary

## --------------------------------------------------------

## Outcome Frequency Outcome Frequency

## --------------------------------------------------------

## 0 4004 1 517

## --------------------------------------------------------

##

## Maximum Likelihood Estimates

## -----------------------------------------------------------------------

## Parameter DF Estimate Std. Error z value Pr(>|z|)

## -----------------------------------------------------------------------

## (Intercept) 1 -5.1347 0.3728 -13.7729 0.0000

## age 1 0.0096 0.0067 1.4299 0.1528

## duration 1 0.0042 2e-04 20.7853 0.0000

## previous 1 -0.0357 0.0392 -0.9089 0.3634

## housingno 1 0.7894 0.1232 6.4098 0.0000

## defaultyes 1 -0.8691 0.6919 -1.2562 0.2091

## loanno 1 0.6598 0.1945 3.3925 7e-04

## poutcomefailure 1 0.6085 0.2012 3.0248 0.0025

## poutcomeother 1 1.1354 0.2700 4.2057 0.0000

## poutcomesuccess 1 3.2481 0.2462 13.1913 0.0000

## jobtechnician 1 -0.2713 0.1806 -1.5019 0.1331

## jobentrepreneur 1 -0.7041 0.3809 -1.8486 0.0645

## jobblue-collar 1 -0.6132 0.1867 -3.2851 0.0010

## jobunknown 1 -0.9932 0.8226 -1.2073 0.2273

## jobretired 1 0.3197 0.2729 1.1713 0.2415

## jobadmin. 1 0.1120 0.2001 0.5599 0.5755

## jobservices 1 -0.1750 0.2265 -0.7728 0.4397

## jobself-employed 1 -0.1408 0.3009 -0.4680 0.6398

## jobunemployed 1 -0.6581 0.3432 -1.9174 0.0552

## jobhousemaid 1 -0.7456 0.3932 -1.8963 0.0579

## jobstudent 1 0.1927 0.3433 0.5613 0.5746

## maritalsingle 1 0.5451 0.1387 3.9299 1e-04

## maritaldivorced 1 -0.1989 0.1986 -1.0012 0.3167

## -----------------------------------------------------------------------

##

## Association of Predicted Probabilities and Observed Responses

## ---------------------------------------------------------------

## % Concordant 0.8886 Somers' D 0.7773

## % Discordant 0.1114 Gamma 0.7773

## % Tied 0.0000 Tau-a 0.1575

## Pairs 2070068 c 0.8886

## ---------------------------------------------------------------If you want to examine the odds ratio estimates, set odd_conf_limit to TRUE.

The odds ratio estimates are not explicitly computed as we observed considerable

increase in computation time when dealing with large data sets.

Using Formula

Let us use the model formula and the data set to generate the above results.

blr_regress(y ~ age + duration + previous + housing + default +

loan + poutcome + job + marital, data = bank_marketing)## - Creating model overview.

## - Creating response profile.

## - Extracting maximum likelihood estimates.

## - Estimating concordant and discordant pairs.## Model Overview

## ------------------------------------------------------------------------

## Data Set Resp Var Obs. Df. Model Df. Residual Convergence

## ------------------------------------------------------------------------

## data y 4521 4520 4498 TRUE

## ------------------------------------------------------------------------

##

## Response Summary

## --------------------------------------------------------

## Outcome Frequency Outcome Frequency

## --------------------------------------------------------

## 0 4004 1 517

## --------------------------------------------------------

##

## Maximum Likelihood Estimates

## -----------------------------------------------------------------------

## Parameter DF Estimate Std. Error z value Pr(>|z|)

## -----------------------------------------------------------------------

## (Intercept) 1 -5.1347 0.3728 -13.7729 0.0000

## age 1 0.0096 0.0067 1.4299 0.1528

## duration 1 0.0042 2e-04 20.7853 0.0000

## previous 1 -0.0357 0.0392 -0.9089 0.3634

## housingno 1 0.7894 0.1232 6.4098 0.0000

## defaultyes 1 -0.8691 0.6919 -1.2562 0.2091

## loanno 1 0.6598 0.1945 3.3925 7e-04

## poutcomefailure 1 0.6085 0.2012 3.0248 0.0025

## poutcomeother 1 1.1354 0.2700 4.2057 0.0000

## poutcomesuccess 1 3.2481 0.2462 13.1913 0.0000

## jobtechnician 1 -0.2713 0.1806 -1.5019 0.1331

## jobentrepreneur 1 -0.7041 0.3809 -1.8486 0.0645

## jobblue-collar 1 -0.6132 0.1867 -3.2851 0.0010

## jobunknown 1 -0.9932 0.8226 -1.2073 0.2273

## jobretired 1 0.3197 0.2729 1.1713 0.2415

## jobadmin. 1 0.1120 0.2001 0.5599 0.5755

## jobservices 1 -0.1750 0.2265 -0.7728 0.4397

## jobself-employed 1 -0.1408 0.3009 -0.4680 0.6398

## jobunemployed 1 -0.6581 0.3432 -1.9174 0.0552

## jobhousemaid 1 -0.7456 0.3932 -1.8963 0.0579

## jobstudent 1 0.1927 0.3433 0.5613 0.5746

## maritalsingle 1 0.5451 0.1387 3.9299 1e-04

## maritaldivorced 1 -0.1989 0.1986 -1.0012 0.3167

## -----------------------------------------------------------------------

##

## Association of Predicted Probabilities and Observed Responses

## ---------------------------------------------------------------

## % Concordant 0.8886 Somers' D 0.7773

## % Discordant 0.1114 Gamma 0.7773

## % Tied 0.0000 Tau-a 0.1575

## Pairs 2070068 c 0.8886

## ---------------------------------------------------------------Model Fit Statistics

Model fit statistics are available to assess how well the model fits the data and to compare two different models.The output includes likelihood ratio test, AIC, BIC and a host of pseudo r-squared measures. You can read more about pseudo r-squared at https://stats.idre.ucla.edu/other/mult-pkg/faq/general/faq-what-are-pseudo-r-squareds/.

Single Model

blr_model_fit_stats(model)## Model Fit Statistics

## ----------------------------------------------------------------------------------

## Log-Lik Intercept Only: -1607.330 Log-Lik Full Model: -1123.340

## Deviance(4498): 2246.679 LR(22): 967.980

## Prob > LR: 0.000

## MCFadden's R2 0.301 McFadden's Adj R2: 0.287

## ML (Cox-Snell) R2: 0.193 Cragg-Uhler(Nagelkerke) R2: 0.379

## McKelvey & Zavoina's R2: 0.388 Efron's R2: 0.278

## Count R2: 0.904 Adj Count R2: 0.157

## BIC: 2440.259 AIC: 2292.679

## ----------------------------------------------------------------------------------Model Validation

Hosmer Lemeshow Test

Hosmer and Lemeshow developed a goodness-of-fit test for logistic regression models with binary responses. The test involves dividing the data into approximately ten groups of roughly equal size based on the percentiles of the estimated probabilities. The observations are sorted in increasing order of their estimated probability of having an even outcome. The discrepancies between the observed and expected number of observations in these groups are summarized by the Pearson chi-square statistic, which is then compared to chi-square distribution with t degrees of freedom, where t is the number of groups minus 2. Lower values of Goodness-of-fit are preferred.

blr_test_hosmer_lemeshow(model)## Partition for the Hosmer & Lemeshow Test

## --------------------------------------------------------------

## def = 1 def = 0

## Group Total Observed Expected Observed Expected

## --------------------------------------------------------------

## 1 453 2 5.14 451 447.86

## 2 452 3 8.63 449 443.37

## 3 452 4 11.88 448 440.12

## 4 452 7 15.29 445 436.71

## 5 452 14 19.39 438 432.61

## 6 452 10 24.97 442 427.03

## 7 452 31 33.65 421 418.35

## 8 452 62 49.74 390 402.26

## 9 452 128 88.10 324 363.90

## 10 452 256 260.21 196 191.79

## --------------------------------------------------------------

##

## Goodness of Fit Test

## ------------------------------

## Chi-Square DF Pr > ChiSq

## ------------------------------

## 52.9942 8 0.0000

## ------------------------------Gains Table & Lift Chart

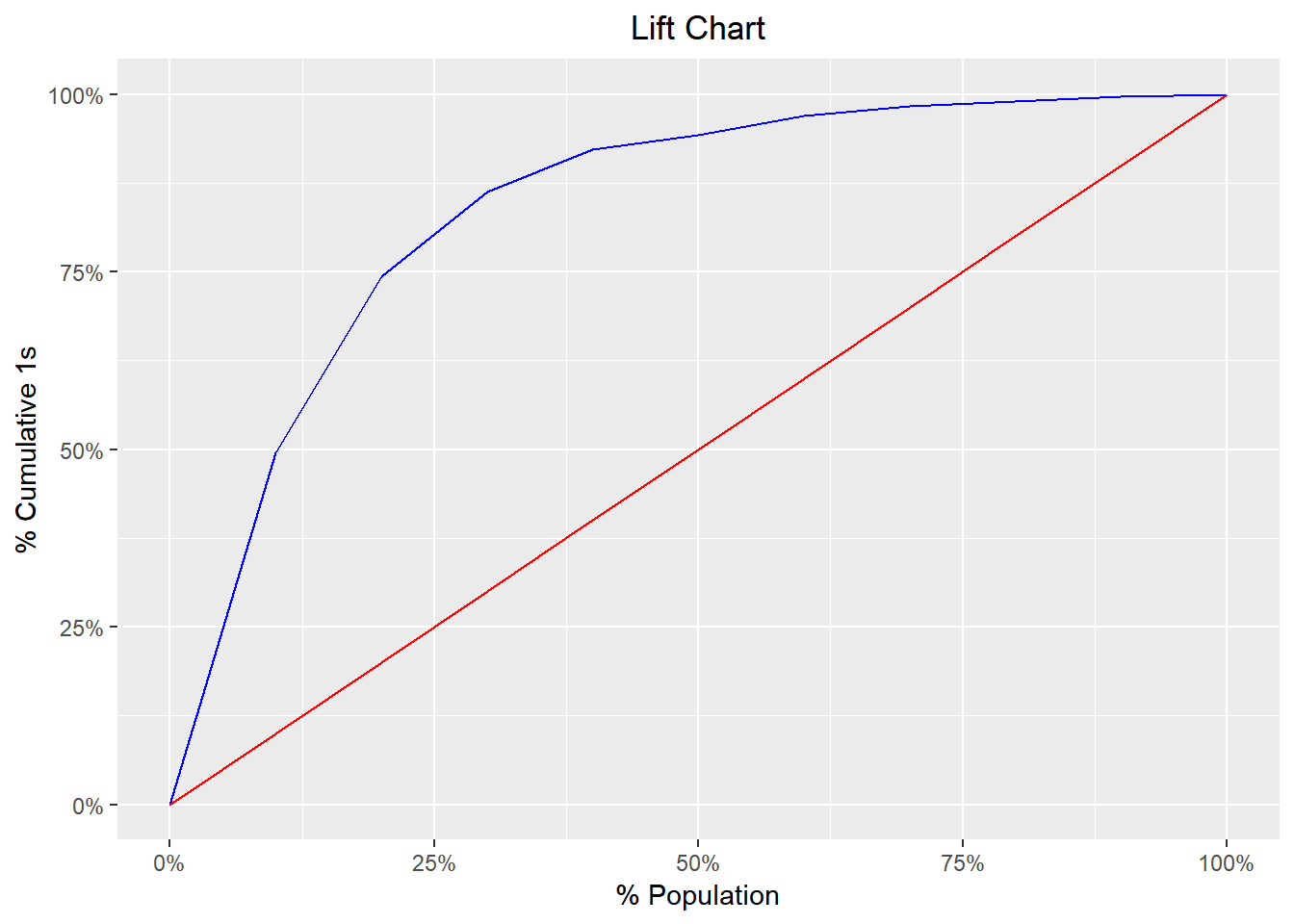

A lift curve is a graphical representation of the % of cumulative events captured at a specific cut-off. The cut-off can be a particular decile or a percentile. Similar, to rank ordering procedure, the data is in descending order of the scores and is then grouped into deciles/percentiles. The cumulative number of observations and events are then computed for each decile/percentile. The lift curve is the created using the cumulative % population as the x-axis and the cumulative percentage of events as the y-axis.

blr_gains_table(model)## # A tibble: 10 x 12

## decile total `1` `0` ks tp tn fp fn sensitivity

## <dbl> <int> <int> <int> <dbl> <int> <int> <int> <int> <dbl>

## 1 1 452 256 196 44.6 256 3808 196 261 49.5

## 2 2 452 128 324 61.3 384 3484 520 133 74.3

## 3 3 452 62 390 63.5 446 3094 910 71 86.3

## 4 4 452 31 421 59.0 477 2673 1331 40 92.3

## 5 5 452 10 442 49.9 487 2231 1773 30 94.2

## 6 6 452 14 438 41.7 501 1793 2211 16 96.9

## 7 7 452 7 445 31.9 508 1348 2656 9 98.3

## 8 8 452 4 448 21.5 512 900 3104 5 99.0

## 9 9 452 3 449 10.9 515 451 3553 2 99.6

## 10 10 453 2 451 0 517 0 4004 0 100

## # ... with 2 more variables: specificity <dbl>, accuracy <dbl>Lift Chart

model %>%

blr_gains_table() %>%

plot()

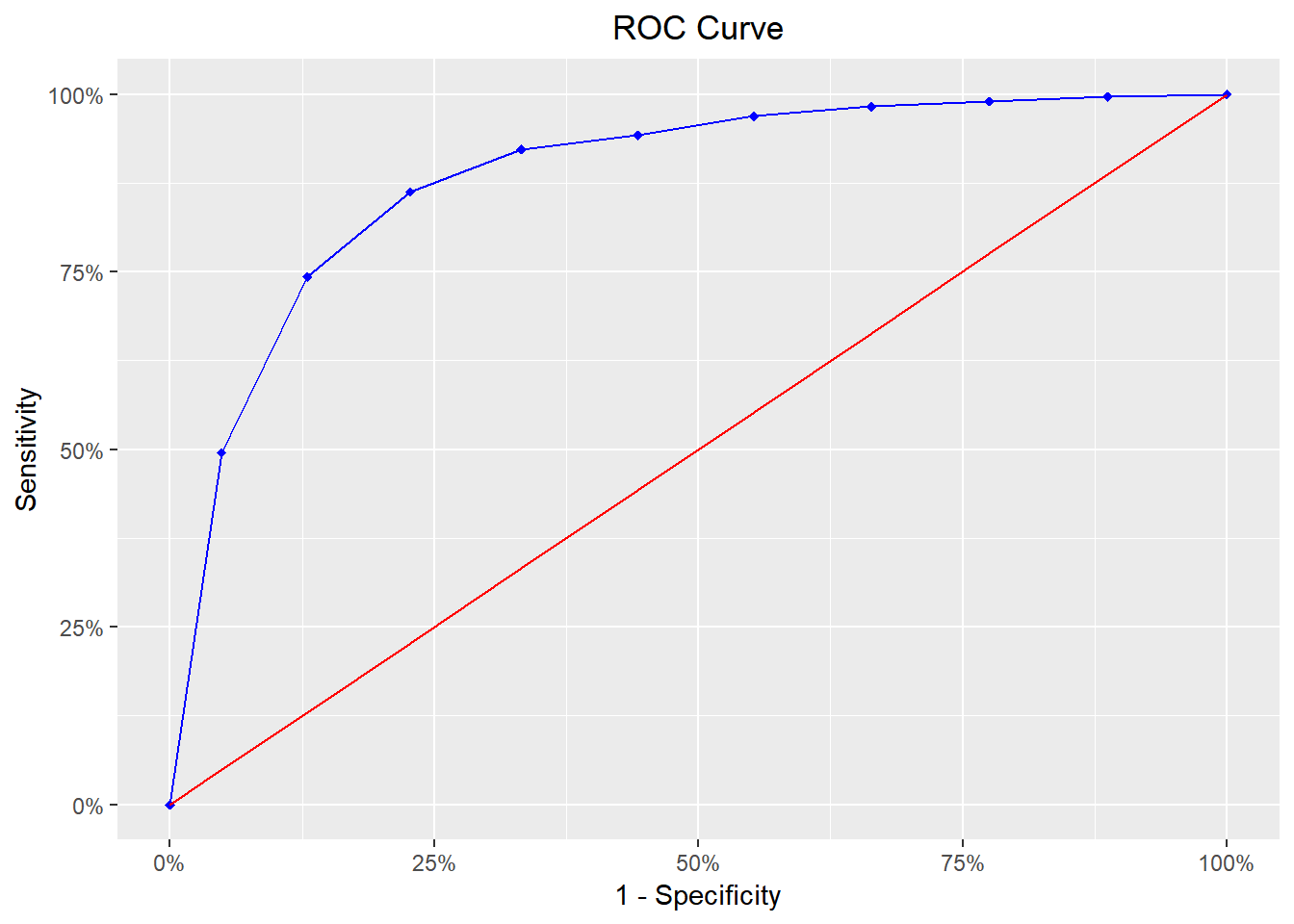

ROC Curve

ROC curve is a graphical representation of the validity of cut-offs for a logistic regression model. The ROC curve is plotted using the sensitivity and specificity for all possible cut-offs, i.e., all the probability scores. The graph is plotted using sensitivity on the y-axis and 1-specificity on the x-axis. Any point on the ROC curve represents a sensitivity X (1-specificity) measure corresponding to a cut-off. The area under the ROC curve is used as a validation measure for the model – the bigger the area the better is the model.

model %>%

blr_gains_table() %>%

blr_roc_curve()

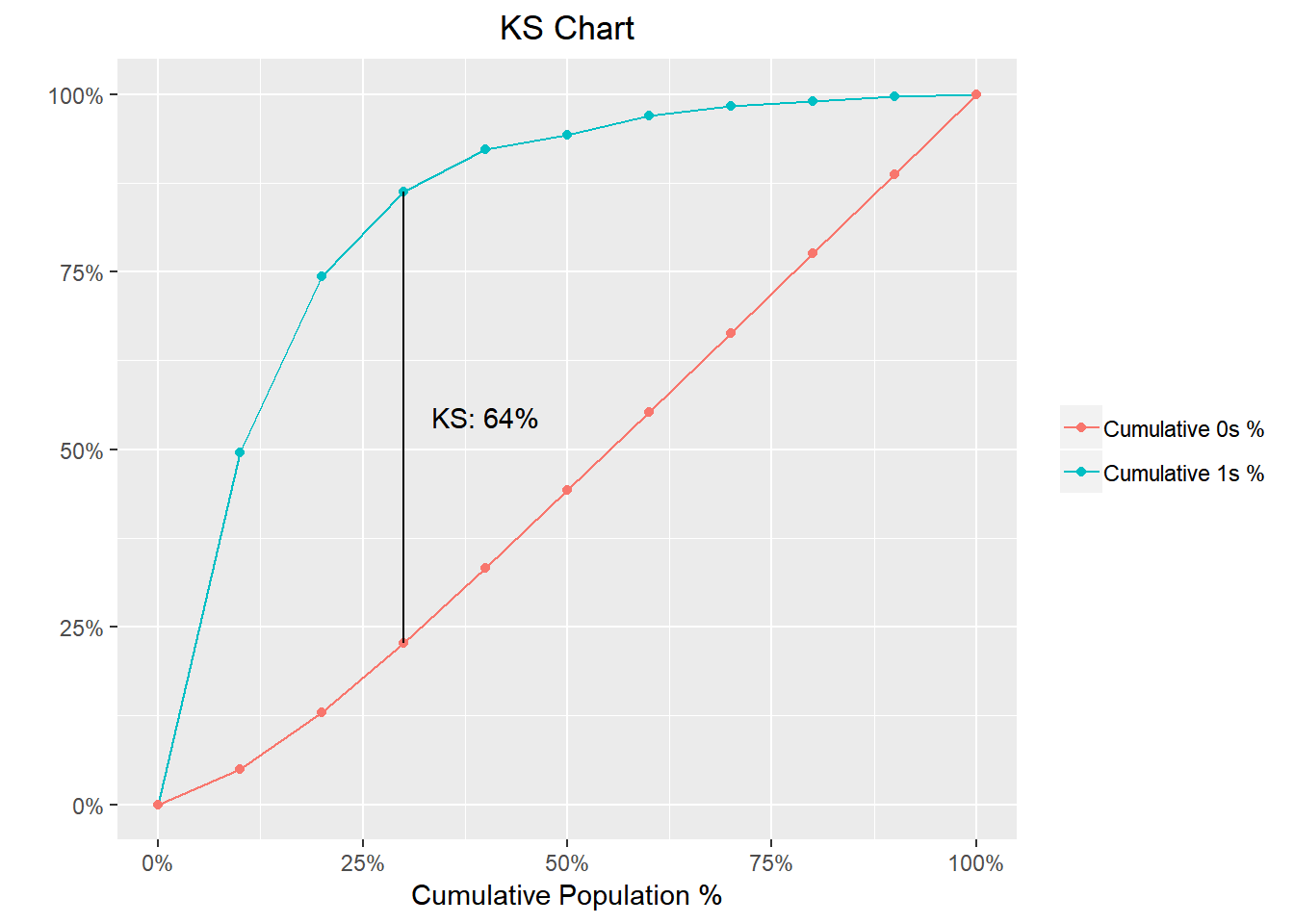

KS Chart

The KS Statistic is again a measure of model efficiency, and it is created using the lift curve. The lift curve is created to plot % events. If we also plot % non-events on the same scale, with % population at x-axis, we would get another curve. The maximum distance between the lift curve for events and that for non-events is termed as KS. For a good model, KS should be big (>=0.3) and should occur as close to the event rate as possible.

model %>%

blr_gains_table() %>%

blr_ks_chart()

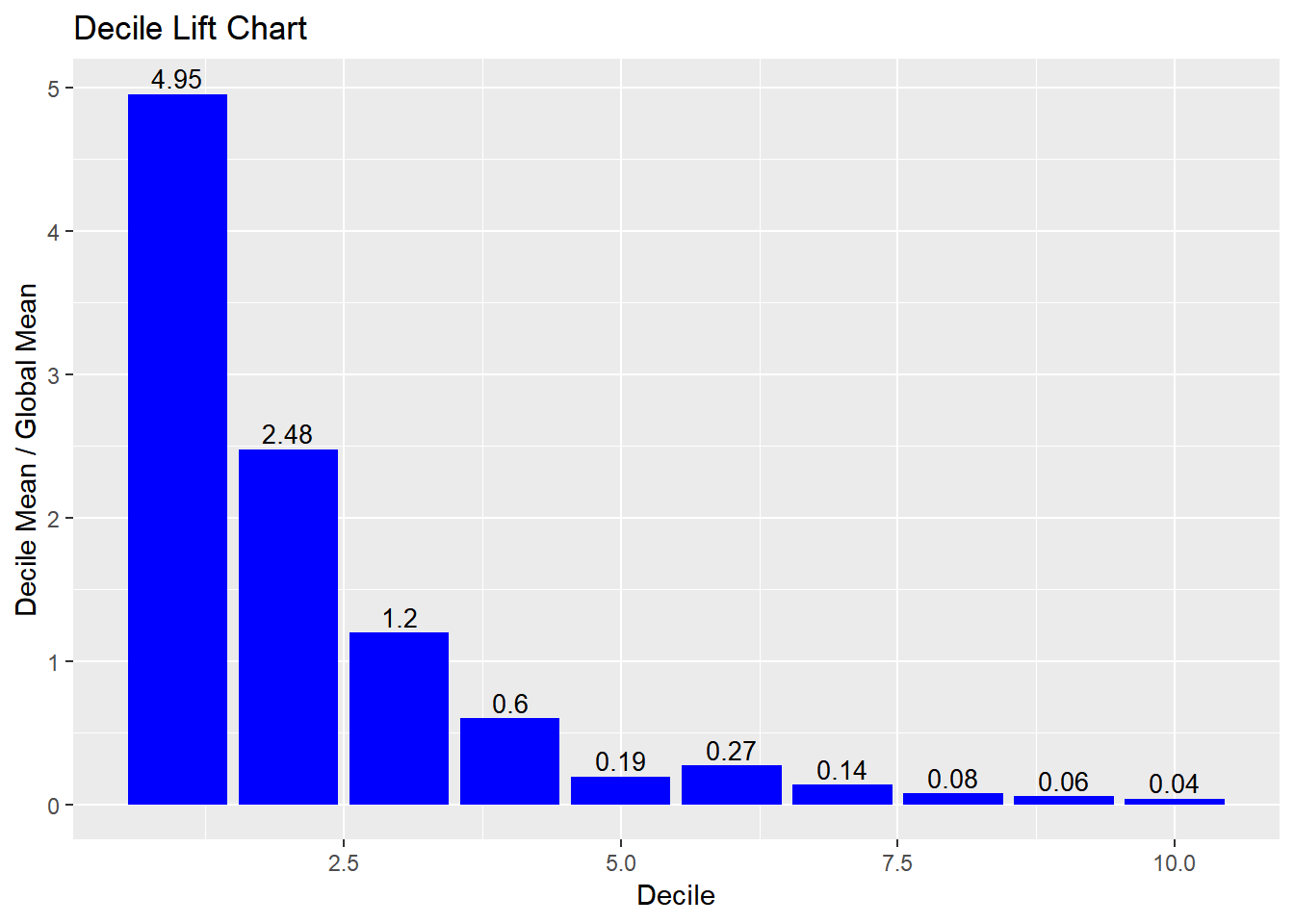

Decile Lift Chart

The decile lift chart displays the lift over the global mean event rate for each decile. For a model with good discriminatory power, the top deciles should have an event/conversion rate greater than the global mean.

model %>%

blr_gains_table() %>%

blr_decile_lift_chart()

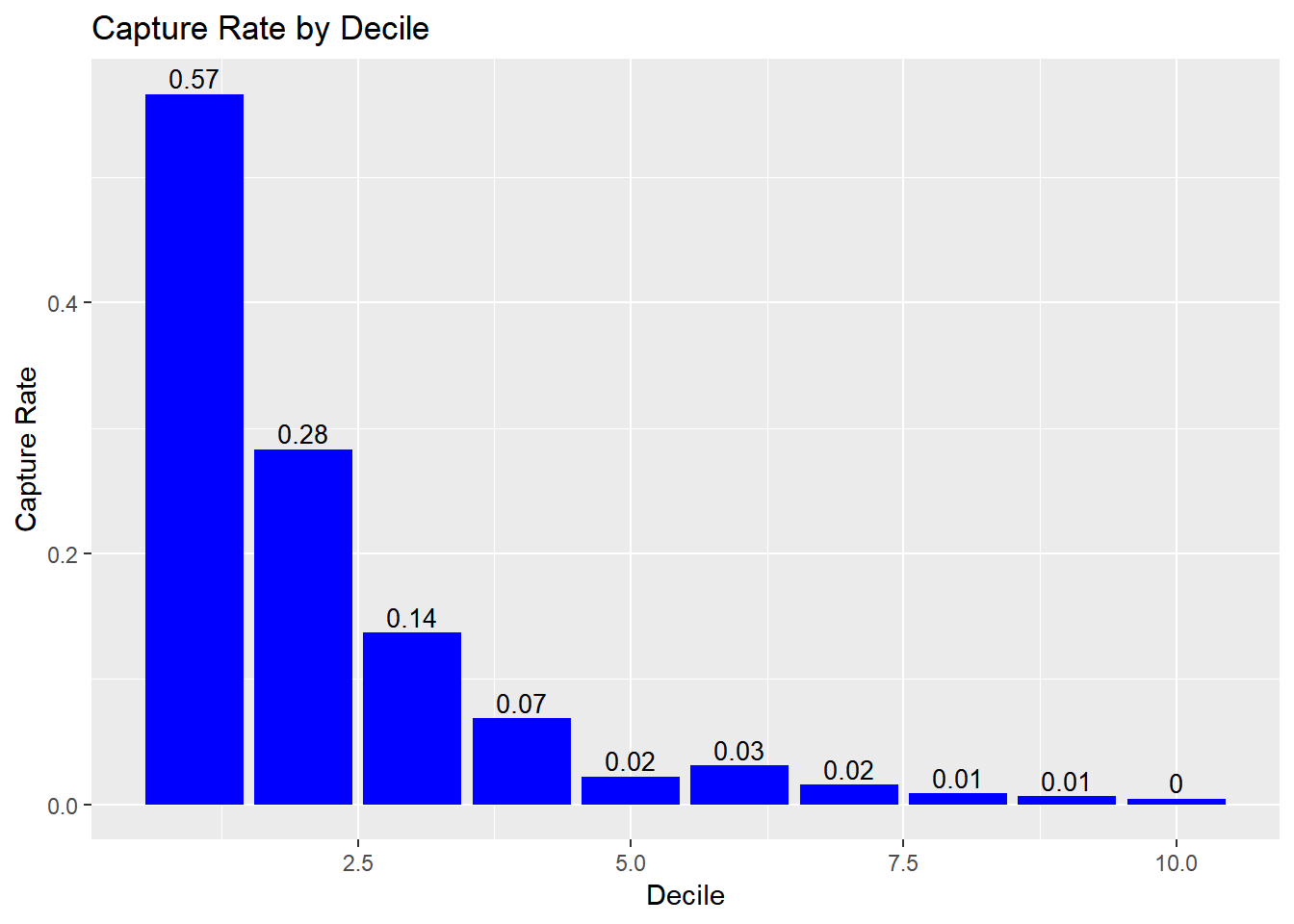

Capture Rate by Decile

If the model has good discriminatory power, the top deciles should have a higher event/conversion rate compared to the bottom deciles.

model %>%

blr_gains_table() %>%

blr_decile_capture_rate()

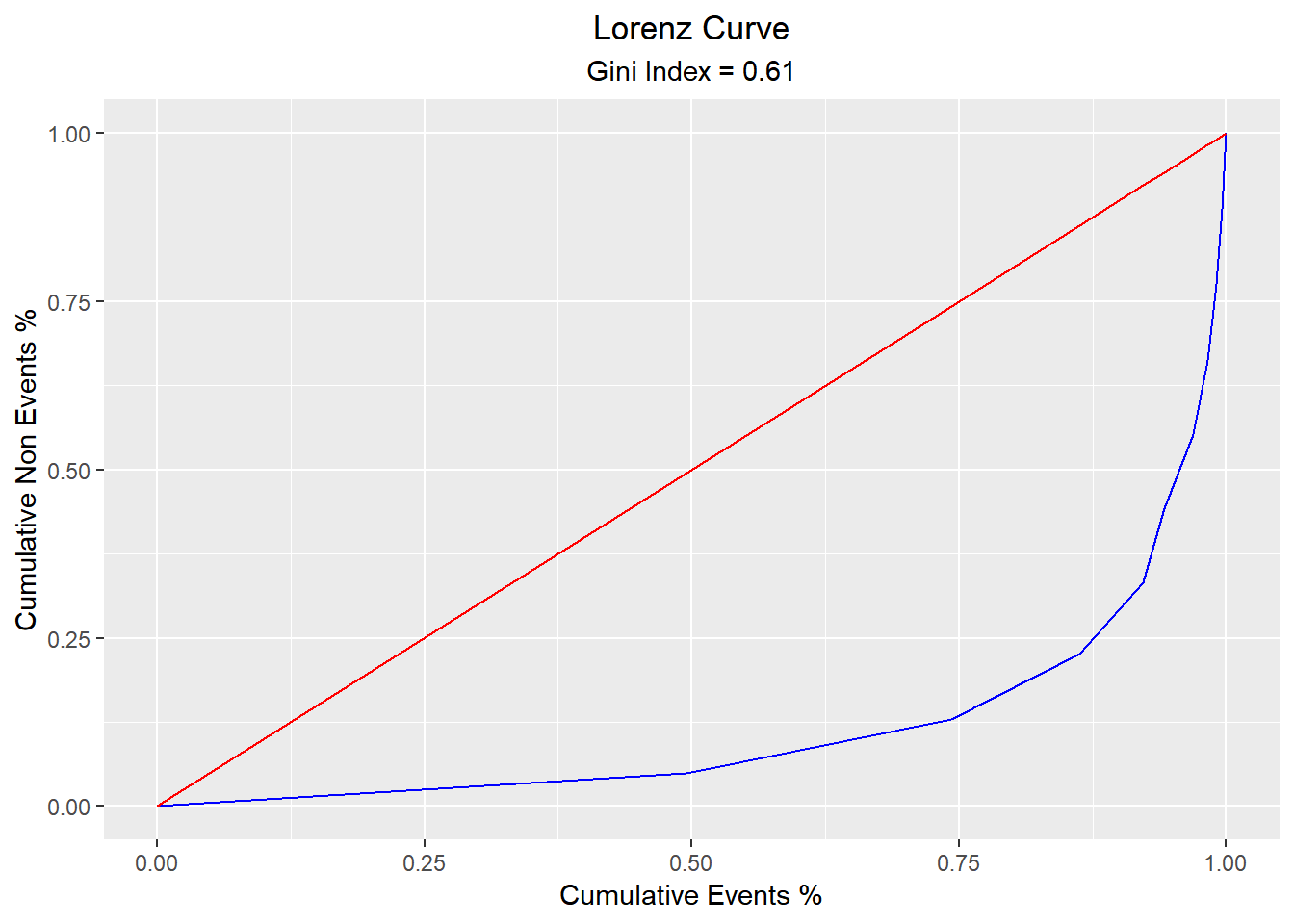

Lorenz Curve

The Lorenz curve is a simple graphic device which illustrates the degree of inequality in the distribution of thevariable concerned. It is a visual representation of inequality used to measure the discriminatory power of the predictive model.

blr_lorenz_curve(model)

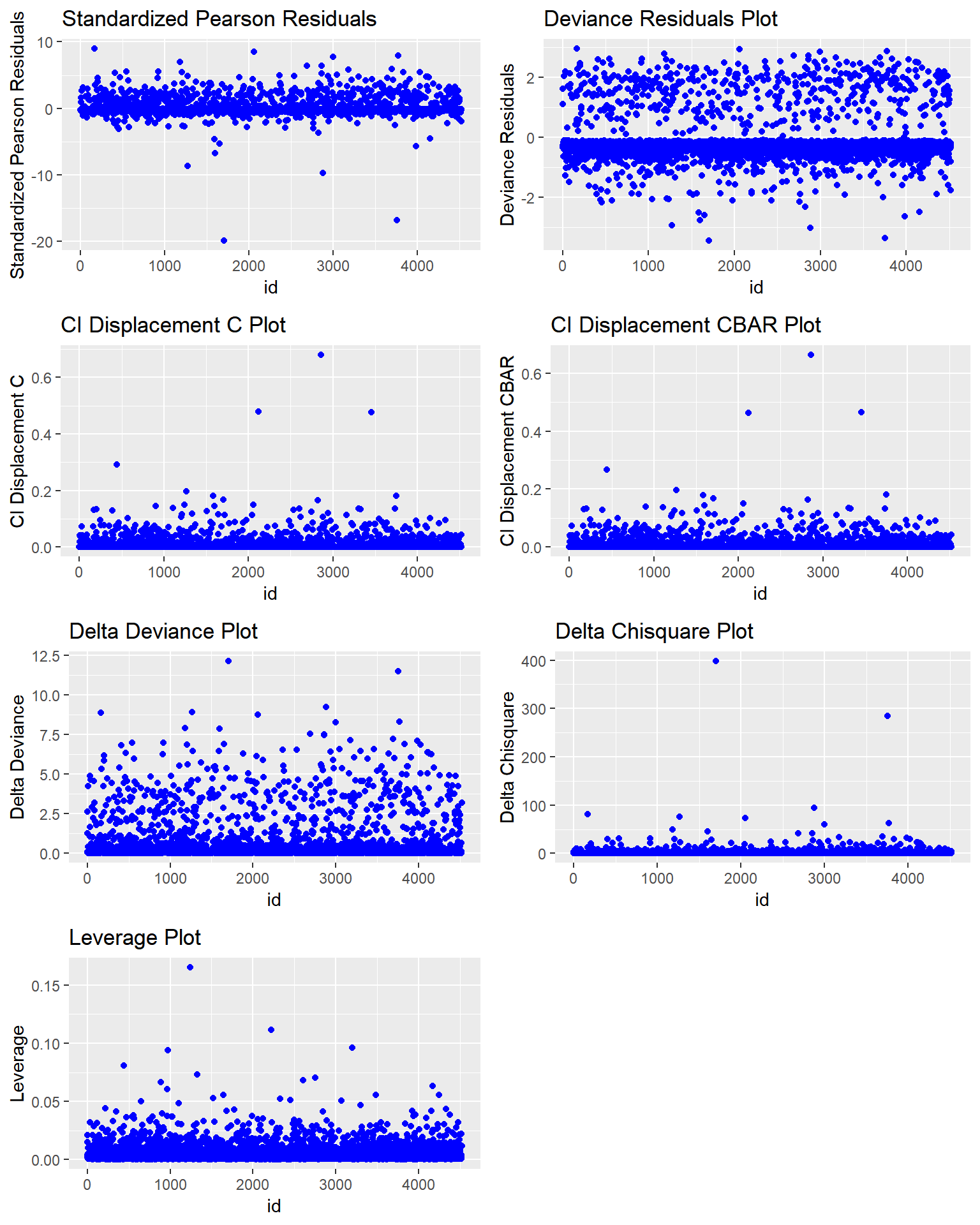

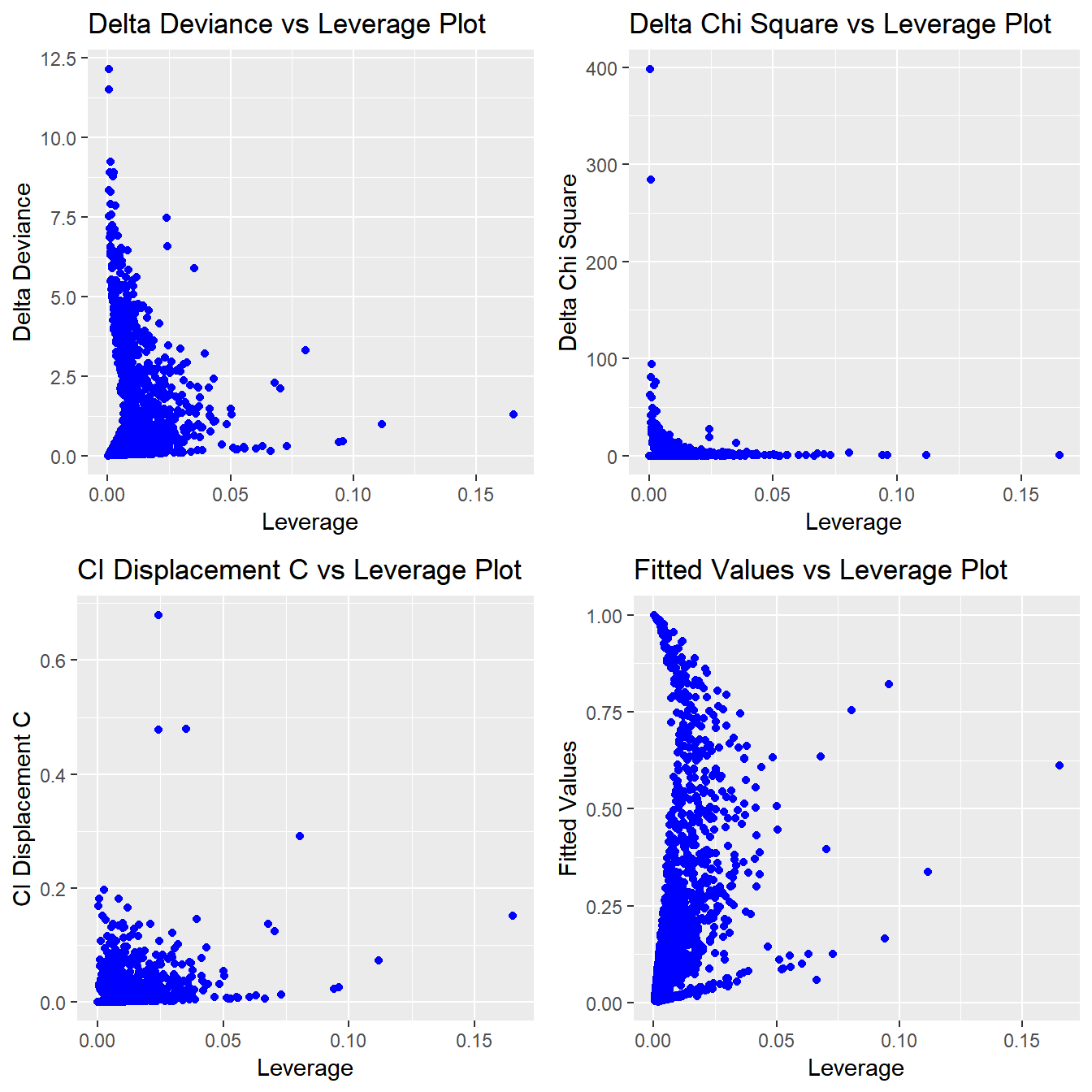

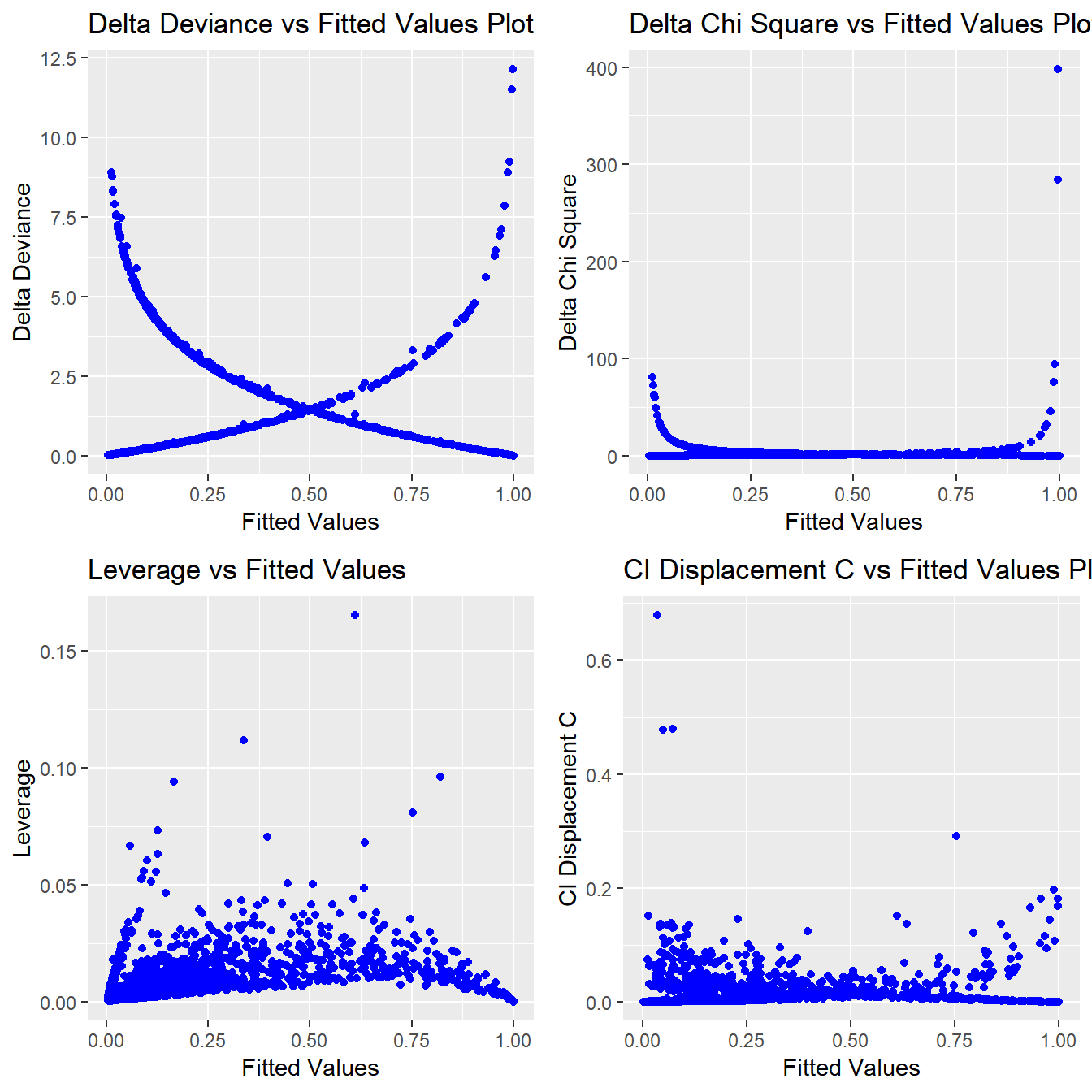

Residual & Influence Diagnostics

blorr can generate 22 plots for residual, influence and leverage diagnostics.

Influence Diagnostics

blr_plot_diag_influence(model)

Leverage Diagnostics

blr_plot_diag_leverage(model)

Fitted Values Diagnostics

blr_plot_diag_fit(model)

Learning More

The blorr website includes comprehensive documentation on using the package, including the following article that covers various aspects of using blorr.

Feedback

All feedback is welcome. Issues (bugs and feature requests) can be posted to github tracker. For help with code or other related questions, feel free to reach me hebbali.aravind@gmail.com.